Key Takeaways

- Know Your Rights: Borrowers in Singapore are protected under the Moneylenders Act, and understanding your rights can help you identify when it’s necessary to file a complaint against a money lender.

- Recognise Misconduct: Unfair practices, overcharging fees, or licensed money lender harassment are valid grounds for a formal complaint.

- Follow the Proper Channels: Report issues to the right authority—regulatory breaches to the Registry of Moneylenders, harassment to the police, and contractual disputes to the Small Claims Tribunal.

- Document Everything: Keeping your loan agreements, payment receipts, and all communication records strengthens your money lender report and improves the chances of a successful resolution.

Dealing with a licensed money lender can be stressful, especially when something feels off or doesn’t go as expected. The good news? Borrowers in Singapore are well protected by law, and there are legitimate avenues for lodging a complaint against a licensed money lender. Some reasons why filing a money lender report may be necessary include harassment by licensed money lenders and contractual disputes.

Similarly, it’s crucial to take the right steps if you’re dealing with an unlicensed money lender.

Whether you have a nagging feeling of being treated unfairly by your lender or just want to know how to file a complaint against a money lender, this guide is for you.

Understanding Licensed vs Unlicensed Money Lenders

| Licensed Money Lenders | Unlicensed Money Lenders (Loan Sharks or Ah Longs) |

|---|---|

| ✔️ Regulated under the Moneylenders Act | ❌ Operate illegally outside of the law |

| ✔️ Listed on MinLaw’s list of licensed lenders | ❌ No official registration or licensing |

| ✔️ Clear written contracts with terms explained in a language you understand | ❌ No proper contract and vague terms |

| ✔️ Max 4% monthly interest & late interest; S$60 late fee/month; 10% admin fee | ❌ Extremely high or hidden interest rates & fees |

| ✔️ No unsolicited ads or loan offers via WhatsApp/Telegram, SMS, or social media | ❌ Often contacts borrowers via unsolicited messages |

| ✔️ Debt recovery through formal channels only | ❌ Often use harassment, threats, violence or intimidation |

It’s always a good idea to double-check the licence status of the lender before proceeding with a loan. If the loan offer sounds too good to be true or something feels strange, give it a miss!

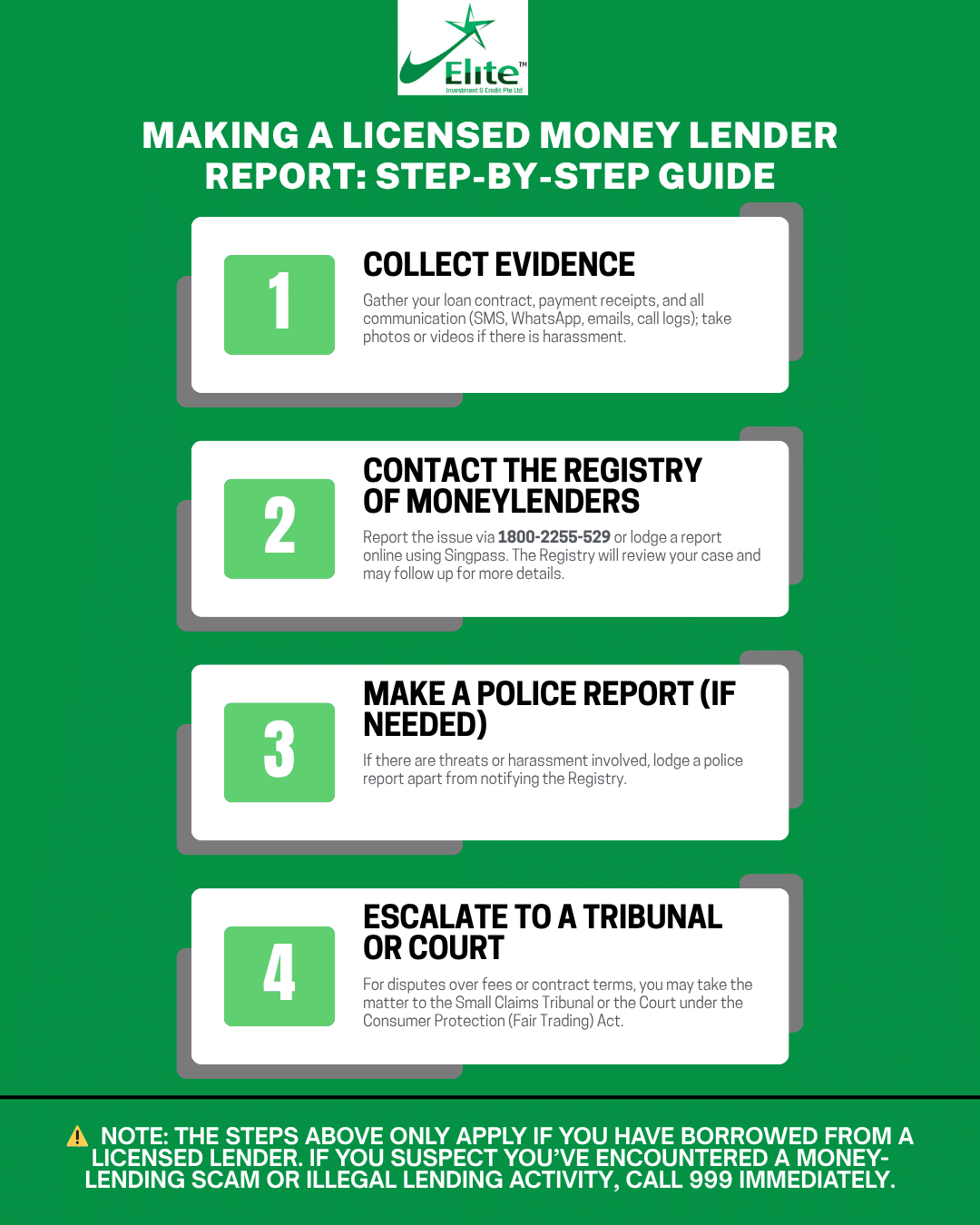

How to File a Complaint Against a Licensed Money Lender in Singapore

When to Lodge a Money Lender Report: Knowing Your Rights as a Borrower

As a borrower in Singapore, you’re protected by the Moneylenders Act (but only when you borrow from licensed lenders). Licensed money lenders aren’t allowed to engage in abusive or misleading behaviour—they can’t threaten you, spring hidden fees, or trick you with unclear contracts. Knowing what counts as harassment or unfair practices can help you decide when it’s time to file a complaint against a licensed money lender.

What Counts as Reportable Misconduct

You should consider lodging a complaint against a licensed money lender if you experience:

- Threats or intimidation: Shouting, abusive language, or showing up at your home unnecessarily

- Too many calls or messages: Repeated calls or texts outside of permitted hours (Mon-Fri: 8 am-10 pm; Weekends or Public Holidays: 9 am-9 pm)

- Hidden or excessive charges: Charging fees above the legal limits

Contract issues: Failing to provide you with a written copy of the signed loan agreement, payment receipts, or clear explanations of loan terms.

What Happens After You Make a Licensed Money Lender Report

Once you submit a money lender report, the Registry will review your case and may reach out if it needs more information. If a licensed lender is found to have violated the rules, the Registry will take enforcement action, ranging from issuing warnings and fines to suspending or revoking their licence. Rest assured that your complaint will be kept strictly confidential unless you consent to disclosure.

3 Quick Checks to Protect Yourself From Money Lender Harassment

- Always verify the lender’s licence status via the Registry of Moneylenders before sharing any personal information. This protects you from loan scams and unlicensed operators.

- Read the fine print carefully. Make sure you understand every detail of the contract, including interest rates, fees, and repayment schedules. Check that all charges comply with legal caps to avoid trouble later on.

- Ask questions and watch for warning signs. If any clause in the agreement is confusing or the lender hesitates to explain, it’s a red flag—walk away and look for a transparent and trustworthy lender instead.

Borrow Confidently With Elite Investment & Credit

At Elite Investment & Credit, ethical lending isn’t just a promise—it’s a commitment backed by full compliance with Singapore’s moneylending regulations. With transparent contracts, crystal clear communication, and fair practices, you can move forward with peace of mind knowing you’re dealing with a trusted licensed lender.

Ready to take the next step? Apply now or contact us to get started right away.