What is a licensed money lender in Singapore?

How old do I have to be to get a loan from a legal money lender in Singapore?

Are all authorised money lenders the same?

Do licensed money lenders in Singapore have high loan approval rates?

Do legal money lenders offer personalised loan solutions?

Can I apply for a licensed money lender loan online?

Can I negotiate for flexible repayment terms with a licensed money lender?

Is there any income requirement I must hit in order to borrow from a legal money lender?

Is there any minimum amount for a licensed money lender loan?

Do legal money lenders offer prompt customer service?

Do licensed money lenders provide financial advice?

Is it possible to get my loan from a legal money lender approved if my credit rating is poor?

Can I still get a loan if I can’t make it to your registered money lender office during business hours?

What are the modes of payment available for my money lender loan?

Can I take up a legal loan from you even though I’m a discharged bankrupt?

How do I tell the difference between a licensed money lender and an illegitimate money lender in Singapore?

What is the difference between taking a loan from local money lenders and banks?

What should I look out for when enquiring with private money lenders?

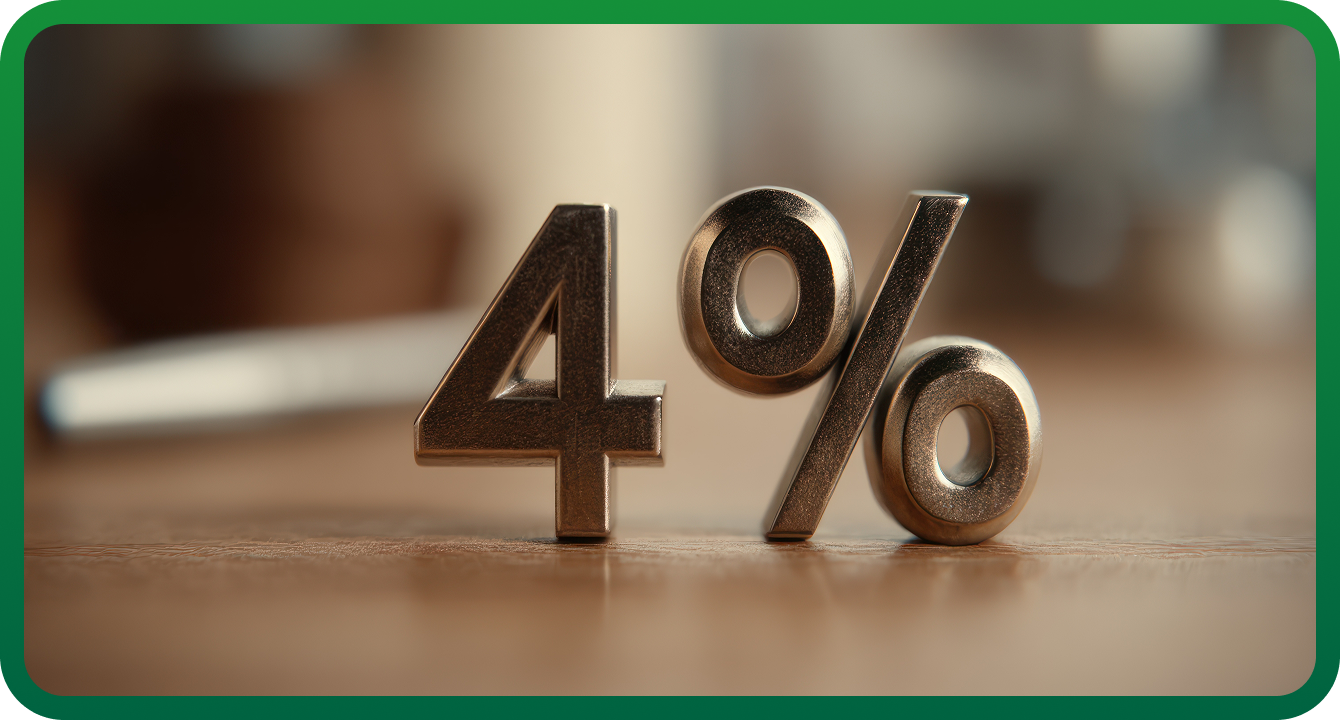

What are the interest rates, fees, and charges when borrowing from licensed money lenders?

Do money lenders levy early repayment charges?

How can I improve my chances of a successful loan application with a licensed money lender in Singapore?

What scenarios might a legal money lender reject my loan application?

What should I take note of when borrowing from licensed money lenders in Singapore?

What are some loan repayment tips to pay off licensed money lender loans on time?

What happens if you are unable to pay a money lender in Singapore?

Are licensed money lenders allowed to harass borrowers?

How to deal with licensed money lender harassment in Singapore?