Furniture not only makes your home functional but also reflects your tastes and style. However, furnishing a home doesn’t come cheap, which can pose a problem to homeowners with smaller budgets. Fortunately, you can use a furniture loan in Singapore to help you create the home of your dreams.

Where to find a furniture loan in Singapore?

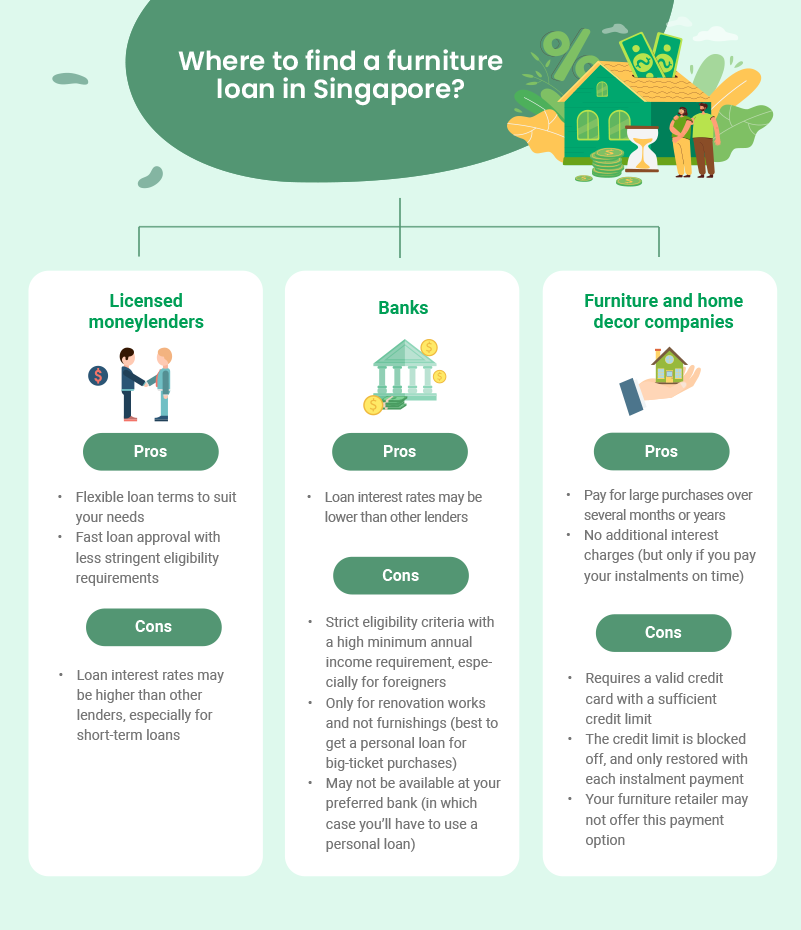

| Licensed moneylenders | – Furniture loan

– Short-term loan |

| Banks | – Bundled with a renovation loan

– Personal loan |

| Furniture and home decor companies | – Credit card 0% interest instalment |

Licensed moneylenders

Pros

- Flexible loan terms to suit your needs

- Fast loan approval with less stringent eligibility requirements

Cons

- Loan interest rates may be higher than other lenders, especially for short-term loans

A legal money lender is a popular choice for getting a furniture loan in Singapore. This is because licensed moneylenders are focused on providing flexible loan solutions to meet the needs of a wide swathe of borrowers.

You can approach several licensed moneylenders in Singapore to discuss the terms of your loan, including how much you need, and how long you can take to pay the loan back.

Also, for those who urgently need to buy some new furniture, some licensed moneylenders may provide a short-term loan that can be paid back quickly. However, the loan interest rates for this type of loan are typically higher.

Banks

Pros

- Loan interest rates may be lower than other lenders

Cons

- Strict eligibility criteria with a high minimum annual income requirement, especially for foreigners

- Only offered with a renovation loan

- May not be available at your preferred bank (in which case you’ll have to use a personal loan)

Banks offer a variety of unsecured loans, but you may be hard-pressed to find a loan specifically tailored to home furnishings.

This is because banks that do offer furniture loans (not all banks do) tend to bundle them together with a renovation loan, so you can’t apply for one separately.

Instead, you’ll likely be offered a personal loan to buy your furniture. This can work too, but the interest rates are likely to be higher than a renovation loan.

Renovation loans are among the best choices for homeowners, given their low interest rates. But, you can only use them for built-in furnishings like wardrobes and cabinets, and not for free-standing furniture such as dining tables and sofa sets.

Note that both renovation loans and personal loans will require you to satisfy the bank’s minimum annual income requirement and other eligibility criteria.

Furniture and home decor companies

Pros

- Pay for large purchases over several months or years

- No additional interest charges (but only if you pay your instalments on time)

Cons

- Requires a valid credit card with a sufficient credit limit

- The credit limit is blocked off, and only restored with each instalment payment

- Your furniture retailer may not offer this payment option

This third option isn’t really a furniture loan per se, but it can allow you to pay for your home furniture purchases over separate instalments, just like you would with a loan.

Many furniture shops and home decor companies provide 0% Instalment Payment Plans (0% IPP) in partnership with credit card issuers.

How this works is your bank pays for the entire sum of your purchase to the merchant first, then it charges an instalment payment each month to your credit card. As advertised, there is no additional interest charged on these instalments.

So what’s the catch? Well, firstly, you’ll need to make sure you keep up with these monthly payments. Failing to do so will incur interest charges equivalent to your bank’s prevailing rate, typically 26% to 29% per annum.

Secondly, your credit limit will be lowered by the value of your purchase, and will only be restored with each instalment you pay back. As such, you’ll need to budget around a lower credit limit while the IPP is still in force.

This also means that you’ll need a credit card with a high enough credit limit to cover your entire furniture purchase in the first place (or have to split your purchase over two or more cards.)

As such, this option is only suitable for those with credit cards, and with high-enough credit limits.

Conclusion: Which furniture loan in Singapore should you choose?

We’ve explored three different options for funding your furniture purchases.

Perhaps the best option, from a money-saving standpoint, is to use a credit card’s 0% IPP, as this would allow you to avoid added interest, while still splitting up your furniture purchase over several instalments. However, this option is unsuitable for those who do not have credit cards, or a high-enough credit limit.

Bank renovation loans can only be used for built-in furniture (and only then, as part of a verified home renovation), while personal loans have higher interest rates. Both types of loans also have strict eligibility criteria and are subject to loan limits.

In comparison, short-term loans and furniture loans from a licensed moneylender in Singapore are likely to be less restrictive (although still subject to rules and regulations) and come with more flexible terms. However, these loans are likely to have the highest interest rates out of the three.

If you need a furniture loan, we can help. Elite Investment and Credit offers furniture loans with flexible terms, fast loan approval, and attractive interest rates to help homeowners all over Singapore achieve the home of their dreams. Apply for your furniture loan today!